Evo Morales, tenant of the Palacio de Quemado for 13 long years now, rejected the fact that 51.3% of Bolivians voted “No” in the 2016 referendum for his fourth presidential candidacy in October 2019. To do so, the Constitutional Court ruled that the same Constitution Morales passed in 2009, which limited presidential reelections, violated his political right to run for office. The ruling stated that term limits were essentially a human rights violation, and, therefore, overruled the Constitution to allow Morales to run for reelection. Now, with all the resources of the state in his favor, Morales will be the candidate of the governing party once again. His reelection in 2014 and the 2006 Constituent Assembly have been questioned as well. However, some disregard these criticisms based on the economic and social achievements of Morales’ administration.

The following piece is a critical analysis of Bolivia’s macroeconomic outlook. Expansive policies – fiscal, monetary and wage policies – and an artificially sustained fixed exchange rate maintain the Bolivian economic growth while sacrificing the macroeconomic stability. These policies lead to a substantial increase in public debt, fiscal and current account deficits, and a notable loss of international reserves.

The Bolivian economy grew an average of 4.9% between 2006 and 2017 and 4.5% in 2018 according to IMF estimates. However, today, Bolivia is not growing mainly due to the commodity boom as it once did until 2014, but rather due to expansionary policies.

The Central Bank of Bolivia (BCB) is not independent from the executive branch and offers credit to provinces and municipalities, as well as payments to government social programs. Undermining the country’s monetary policy autonomy and credibility, the BCB started loaning to state-owned enterprises in 2011, and these loans already represented 12.7% of GDP by 2017. Among the expansive monetary policies of the BCB are lowering the reference rate; reducing reserve ratios; increasing the limit on investment of pension funds in financial institutions; anticipating redemptions of debt securities, and reducing the offer and frequency of auctions of such securities. In the first half of 2018, 516 million Bolivianos (national currency: Bs) was paid in advance to debt holders and the frequency of debt securities auctions went from weekly to bimonthly. Similarly, the BCB went from offering Bs2 billion in debt securities in January 2017 to Bs350 million in June 2018. As a result, the BCB has reduced its stock of securities from Bs25 billion in March 2015 to Bs2 billion in June 2018.

As a result, the money supply grew exponentially (Figures 1 and 2). The fixed nominal exchange rate since 2011 – Bs6.91: US$1 -, and GDP growth itself have kept inflation under control. However, once debt capacities and international reserves are exhausted, the fiscal and current account deficits will make the artificial nominal exchange rate collapse, and then, among other market forces, inflation takes hold.

The last year of fiscal surplus was 2013 (0.6% of GDP). Since then, the fiscal deficit has not stopped growing, reaching 7.8% of GDP in 2017. Consequently, it is not surprising if public expenditure, and therefore the deficit, increases considerably during 2019 due to the presidential elections in October. It is illustrative to see how the Bolivian government increased public spending as a percentage of GDP while the economy decelerated (Figure 3), and how the gap between public expenditures and revenues widened at the same time (Figure 4). This is partly due to the rise of public sector wages, which increased by about 4.0% of GDP from 2006 to 2015 and by 2016 represented approximately 11.2% of GDP when the Latin American average was 8%.

It is important to underline that according to the Inter-American Development Bank, the inefficiency of public spending (6.3% of GDP) is among the highest in the region, only exceeded by Argentina and El Salvador.

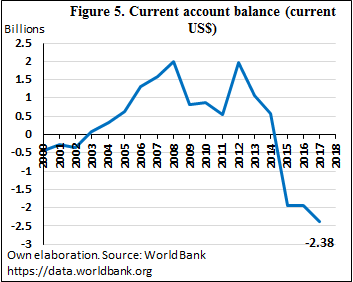

The current account deficit was 6.34% of GDP in 2017, representing US$2.38 billion (Figure 5). Bolivia has gas export contracts with Brazil (until 2019) and Argentina, and 45% of total exports are concentrated on these two countries alone. In 2018 (January-November), Bolivia exported to Argentina and Brazil 36% less than the quotas agreed upon in these contracts. Today, Argentina is asking Bolivia to renegotiate quotas in order to buy less gas, while Jair Bolsonaro’s election in Brazil jeopardizes the ratification of the treaty.

The current account deficit was 6.34% of GDP in 2017, representing US$2.38 billion (Figure 5). Bolivia has gas export contracts with Brazil (until 2019) and Argentina, and 45% of total exports are concentrated on these two countries alone. In 2018 (January-November), Bolivia exported to Argentina and Brazil 36% less than the quotas agreed upon in these contracts. Today, Argentina is asking Bolivia to renegotiate quotas in order to buy less gas, while Jair Bolsonaro’s election in Brazil jeopardizes the ratification of the treaty.

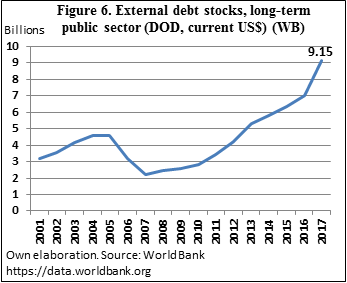

Fiscal and current account deficits have been financed by the BCB through credit to state-owned companies as part of expansionary policies, the reduction of international reserves, and the increase of borrowing by the public sector. From 2014 to 2017, total public and external public debts increased from 37% and 17.3% of GDP, to 51.1% and 24.1% respectively. Ever since Morales took office in January 2006, the external public debt has more than doubled (Figure 6), increasing from US$4.58 billion to US$9.94 billion by November 30, 2018, according to the BCB.

Until 2014, the commodity boom allowed Bolivia to accumulate US$15.12 billion in international reserves. By September 30, 2018, the reserves were 42.3% less (US$8.73 billion). While reserves represented 45.5% of GDP in 2014, by 2017 they fell to 27.1%, and by 2023 they are projected to fall to 9.3%. Reserve levels in months of goods and services covered decreased from 14.1 months in 2014, to 9.7 in 2017, and the forecast is 3.8 months by 2023. By 2020, Bolivia will fall below adequate levels of international reserves, according to the IMF.

Faced with this situation, Bolivia’s need to attract fresh foreign currency and foreign direct investment (FDI) does not seem to be the solution in sight. By 2017, FDI represented 1.93% of GDP, well below the average of Latin America and the Caribbean (3.02%). Despite a slight improvement in international commodity prices, as the IMF confirms, legal insecurity, inefficient or cumbersome regulations, low-level corruption, and an outdated Labor Code that dates from 1942 negatively affect FDI growth. For these reasons, in the World Bank’s “Doing Business 2019,” Bolivia lags 156th (score 50.32 out of 100) out of a total of 190 countries in the ranking, while Latin America and the Caribbean have an average score of 58.97. In addition, the outlook for FDI appears to be overshadowed by the risk of protests following the October presidential elections this year.

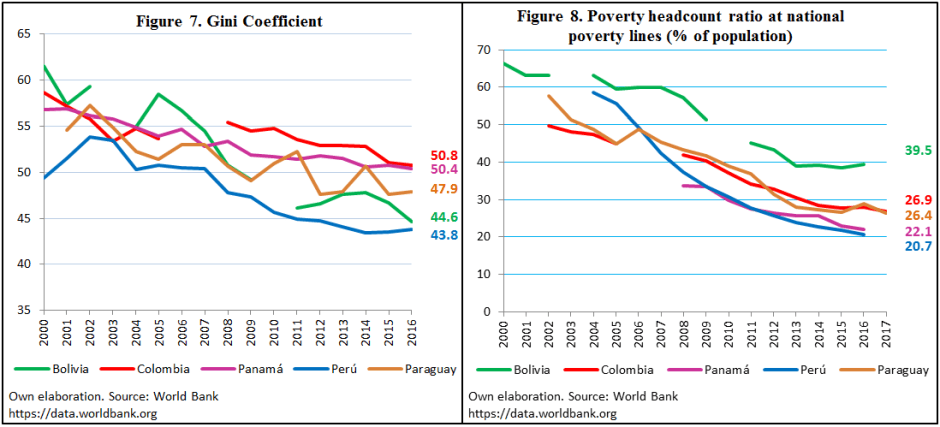

An important remark, while social achievements regarding poverty and inequality reduction are evident, they do not show a different trend from countries of the region (Figures 7, 8, 9, and 10), and still Bolivia faces unresolved issues. One out of five Bolivians is undernourished, which represents the highest rate in Latin America and twice the global ratio.

Morales’ administration has not given any signal of changing its economic policies in the short term. The National Economic and Social Development Plan (PDES), 2016-2020, is a confirmation of the government’s stubborn willingness to continue through the path here analyzed. If Morales is re-elected in October 2019, the trends analyzed here will deepen, or worse, a scenario of crisis similar to 2008 in the Media Luna region could be repeated. The Media Luna region, historically suspicious of its autonomy vis-à-vis the rest of the country, includes the states to the east of Bolivia with the greatest natural and therefore financial resources. These states are Beni, Pando, Santa Cruz, and Tarija. In 2008, the protests that began following the Morales government’s increase in taxes on local hydrocarbon production ended in demands for greater autonomy and even secession from the rest of the country. The social protests and violent confrontations left a dozen dead, losses valued in US$100 million according to the Bolivian government, and diplomatic confrontations between La Paz and Caracas with Washington. In the 2016 referendum, the Media Luna region clearly rejected giving Morales a chance to run again. With the highest percentages of the country, the option “No” surpassed 60% in Santa Cruz, Beni and Tarija, while in Pando this option reached 54%. Macroeconomic mismanagement and social instability are a lethal combination. Venezuela, Morales’ main ally, should serve as the country’s mirror.

Image via Wikipedia

{kind=link}